Nonmonetary Exchange McArthur Inc. has negotiated the purchase of a new piece of automatic12/21/2015 Nonmonetary Exchange McArthur Inc. has negotiated the purchase of a new piece of automatic equipment at a price of $7,000 plus trade-in, f.o.b. factory. McArthur Inc. paid $7,000 cash and traded in used equipment. The used equipment had originally cost $62,000; it had a book value of $42,000 and a secondhand market value of $45,800, as indicated by recent transactions involving similar equipment. Freight and installation charges for the new equipment required a cash payment of $1,100.

(a) Prepare the general journal entry to record this transaction, assuming that the exchange has commercial substance. (b) Assuming the same facts as in (a) except that fair value information for the assets exchanged is not determinable. Prepare the general journal entry to record this transaction.

0 Comments

Sheryl Crow Equipment Company sold 500 Rollomatics during 2008 at $6,000 each.

During 2008, Crow spent $20,000 servicing the 2-year warranties that accompany the Rollomatic. All applicable transactions are on a cash basis. Instructions (a) Prepare 2008 entries for Crow using the expense warranty approach. Assume that Crow estimates the total cost of servicing the warranties will be $120,000 for 2 years. (b) Prepare 2008 entries for Crow assuming that the warranties are not an integral part of the sale. Assume that of the sales total, $150,000 relates to sales of warranty contracts. Crow estimates the total cost of servicing the warranties will be $120,000 for 2 years. Estimate revenues earned on the basis of costs incurred and estimated costs. Conan O Brien Logging and Lumber Company owns 3,000 acres of timberland on the north side of Mount Leno, which was purchased in 2000 at a cost of $550 per acre. In 2012, O Brien began selectively logging this timber tract. In May of 2012, Mount Leno erupted, burying the timberland of O Brien under a foot of ash. All of the timber on the O Brien tract was downed. In addition, the logging roads, built at a cost of $150,000, were destroyed, as well as the logging equipment, with a net book value of $300,000.

At the time of the eruption, O Brien had logged 20% of the estimated 500,000 board feet of timber. Prior to the eruption, O Brien estimated the land to have a value of $200 per acre after the timber was harvested. O Brien includes the logging roads in the depletion base. O Brien estimates it will take 3 years to salvage the downed timber at a cost of $700,000. The timber can be sold for pulp wood at an estimated price of $3 per board foot. The value of the land is unknown, but must be considered nominal due to future uncertainties. Instructions (a) Determine the depletion cost per board foot for the timber harvested prior to the eruption of Mount Leno. (b) Prepare the journal entry to record the depletion prior to the eruption. (c) If this tract represents approximately half of the timber holdings of O Brien, determine the amount of the extraordinary loss due to the eruption of Mount Leno for the year ended December 31, 2012. Purchase of Computer with Zero-Interest-Bearing Debt Napoleon Corporation purchased a computer on December 31, 2009, for $130,000, paying $30,000 down and agreeing to pay the balance in five equal installments of $20,000 payable each December 31 beginning in 2010. An assumed interest rate of 10% is implicit in the purchase price.

(a) Prepare the journal entry (ies) at the date of purchase. (Round to two decimal places) (b) Prepare the journal entry (ies) at December 31, 2010, to record the payment and interest (effective interest method employed). (c) Prepare the journal entry (ies) at December 31, 2011, to record the payment and interest (effective interest method employed). Kathleen Cole Inc. acquired the following assets in January of 2005.

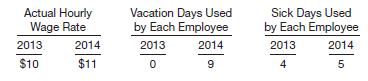

Equipment, estimated service life, 5 years; salvage value, $15,000 ........$525,000 Building, estimated service life, 30 years; no salvage value ...........$693,000 The equipment has been depreciated using the sum-of-the-years-digits method for the first 3 years for financial reporting purposes. In 2008, the company decided to change the method of computing depreciation to the straightline method for the equipment, but no change was made in the estimated service life or salvage value. It was also decided to change the total estimated service life of the building from 30 years to 40 years, with no change in the estimated salvage value. The building is depreciated on the straight-line method. Instructions (a) Prepare the general journal entry to record depreciation expense for the equipment in 2008. (b) Prepare the journal entry to record depreciation expense for the building in 2008. (Round all computations to two decimal places.) Matt Broderick Company began operations on January 2, 2013. It employs 9 individuals who work 8-hour days and are paid hourly. Each employee earns 10 paid vacation days and 6 paid sick days annually. Vacation days may be taken after January 15 of the year following the year in which they are earned. Sick days may be taken as soon as they are earned; unused sick days accumulate. Additional information is as follows. Matt Broderick Company has chosen to accrue the cost of compensated absences at rates of pay in effect during the period when earned and to accrue sick pay when earned. Instructions (a) Prepare journal entries to record transactions related to compensate absences during 2013 and 2014. (b) Compute the amounts of any liability for compensated absences that should be reported on the balance sheet at December 31, 2013 and2014.  Nonmonetary Exchange Alatorre Corporation, which manufactures shoes, hired a recent college graduate to work in its accounting department. On the first day of work, the accountant was assigned to total a batch of invoices with the use of an adding machine. Before long, the accountant, who had never before seen such a machine, managed to break the machine. Alatorre Corporation gave the machine plus $320 to Mills Business Machine Company (dealer) in exchange for a new machine. Assume the following information about the machines.

Alatorre Corp. Mills Co. (Old Machine) (New Machine) Machine cost $290 $270 Accumulated depreciation 140 Fair value 85 405 For each company, prepare the necessary journal entry to record the exchange. (The exchange has commercial substance.) Nonmonetary Exchange Montgomery Company purchased an electric wax melter on April 30, 201112/21/2015 Nonmonetary Exchange Montgomery Company purchased an electric wax melter on April 30, 2011, by trading in its old gas model and paying the balance in cash. The following data relate to the purchase.

List price of new melter $15,800 Cash paid 10,000 Cost of old melter (5-year life, $700 residual value) 12,700 Accumulated depreciation old melter (straight-line) 7,200 Second-hand market value of old melter 5,200 Prepare the journal entry (ies) necessary to record this exchange, assuming that the exchange (a) Has commercial substance, and (b) Lacks commercial substance. Montgomery year ends on December 31, and depreciation has been recorded through December 31, 2010. Acquisition Costs of Realty the expenditures and receipts below and on the next page are related to land, land improvements, and buildings acquired for use in a business enterprise. The receipts are enclosed in parentheses.

(a) Money borrowed to pay building contractor (signed a note) $(275,000) (b) Payment for construction from note proceeds 275,000 (c) Cost of land fill and clearing 10,000 (d) Delinquent real estate taxes on property assumed by purchaser 7,000 (e) Premium on 6-month insurance policy during construction 6,000 (f) Refund of 1-month insurance premium because construction completed early (1,000) (g) Architect fee on building 25,000 (h) Cost of real estate purchased as a plant site (land $200,000 and building $50,000) 250,000 (i) Commission fee paid to real estate agency 9,000 (j) Installation of fences around property 4,000 (k) Cost of razing and removing building 11,000 (l) Proceeds from salvage of demolished building (5,000) (m) Interest paid during construction on money borrowed for construction 13,000 (n) Cost of parking lots and driveways 19,000 (o) Cost of trees and shrubbery planted (permanent in nature) 14,000 (p) Excavation costs for new building 3,000 Identify each item by letter and list the items in columnar form, using the headings shown below. All receipt amounts should be reported in parentheses. For any amounts entered in the Other Accounts column also indicate the accounttitle. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

May 2021

Categories |

RSS Feed

RSS Feed