|

0 Comments

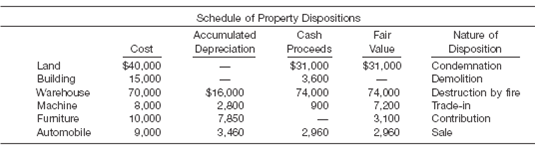

Nonmonetary Exchanges Holyfield Corporation wishes to exchange a machine used in its operations. Holyfield has received the following offers from other companies in the industry. 1. Dorsett Company offered to exchange a similar machine plus $23,000. (The exchange has commercial substance for both parties.) 2. Winston Company offered to exchange a similar machine. (The exchange lacks commercial substance for both parties.) 3. Liston Company offered to exchange a similar machine, but wanted $3,000 in addition to Holyfield machine. (The exchange has commercial substance for both parties.) In addition, Holyfield contacted Greeley Corporation, a dealer in machines. To obtain a new machine, Holyfield must pay $93,000 in addition to trading in its old machine. Holyfield Dorsett Winston Liston Greeley Machine cost $160,000 $120,000 $152,000 $160,000 $130,000 Accumulated depreciation 60,000 45,000 71,000 75,000 Fair value 92,000 69,000 92,000 95,000 185,000 For each of the four independent situations, prepare the journal entries to record the exchange on the books of each company. Classification of Costs and Interest Capitalization On January 1, 2010, Blair Corporation12/20/2015 Classification of Costs and Interest Capitalization On January 1, 2010, Blair Corporation purchased for $500,000 a tract of land (site number 101) with a building. Blair paid a real estate broker commission of $36,000, legal fees of $6,000, and title guarantee insurance of $18,000. The closing statement indicated that the land value was $500,000 and the building value was $100,000. Shortly after acquisition, the building was razed at a cost of $54,000. Blair entered into a $3,000,000 fixed-price contract with Slatkin Builders, Inc. on March 1, 2010, for the construction of an office building on land site number 101. The building was completed and occupied on September 30, 2011. Additional construction costs were incurred as follows. Plans, specifications, and blueprints $21,000 Architects fees for design and supervision 82,000 The building is estimated to have a 40-year life from date of completion and will be depreciated using the 150% declining-balance method. To finance construction costs, Blair borrowed $3,000,000 on March 1, 2010. The loan is payable in 10 annual installments of $300,000 plus interest at the rate of 10%. Blair weighted-average amounts of accumulated building construction expenditures were as follows. For the period March 1 to December 31, 2010 $1,300,000 For the period January 1 to September 30, 2011 1,900,000 (a) Prepare a schedule that discloses the individual costs making up the balance in the land account in respect of land site number 101 as of September 30, 2011. (b) Prepare a schedule that discloses the individual costs that should be capitalized in the office building account as of September 30, 2011. Show supporting computations in good form (AICPA adapted) Dispositions, Including Condemnation, Demolition, and Trade-in Presented below are a schedule of property dispositions for Hollerith Co. The following additional information is available. Land On February 15, a condemnation award was received as consideration for unimproved land held primarily as an investment, and on March 31, another parcel of unimproved land to be held as an investment was purchased at a cost of $35,000. Building On April 2, land and building were purchased at a total cost of $75,000, of which 20% was allocated to the building on the corporate books. The real estate was acquired with the intention of demolishing the building, and this was accomplished during the month of November. Cash proceeds received in November represent the net proceeds from demolition of the building. Warehouse On June 30, the warehouse was destroyed by fire. The warehouse was purchased January 2, 2007, and had depreciated $16,000. On December 27, the insurance proceeds and other funds were used to purchase a replacement warehouse at a cost of $90,000. Machine On December 26, the machine was exchanged for another machine having a fair market value of $6,300 and cash of $900 was received. (The exchange lacks commercial substance.) Furniture On August 15, furniture was contributed to a qualified charitable organization. No other contributions were made or pledged during the year. Automobile On November 3, the automobile was sold to Jared Winger, a stockholder. how these items would be reported on the income statement of Hollerith Co. (AICPAadapted)  Classification of Land and Building Costs Spitfire Company was incorporated on January 2, 201112/20/2015 Disposition of Assets On April 1, 2010, Pavlova Company received a condemnation award of $410,000 cash as compensation for the forced sale of the company land and building, which stood in the path of a new state highway. The land and building cost $60,000 and $280,000, respectively, when they were acquired. At April 1, 2010, the accumulated depreciation relating to the building amounted to $160,000. On August 1, 2010, Pavlova purchased a piece of replacement property for cash. The new land cost $90,000, and the new building cost $380,000.Prepare the journal entries to record the transactions on April 1 and August 1, 2010.

Entries for Disposition of Assets On December 31, 2010, Chrysler Inc. has a machine with a book value of $940,000. The original cost and related accumulated depreciation at this date are as follows.

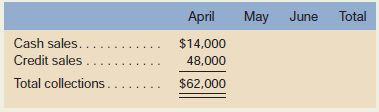

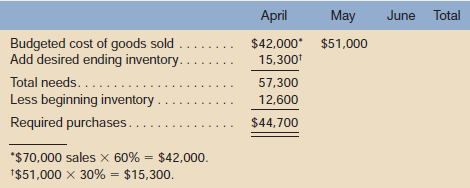

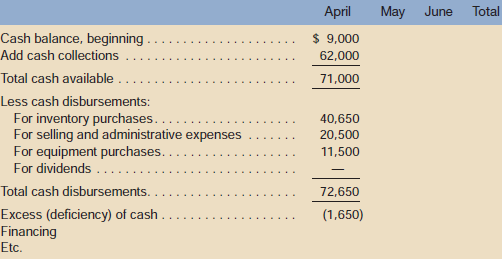

Machine $1,300,000 Accumulated depreciation 360,000 Book value $940,000 Depreciation is computed at $72,000 per year on a straight-line basis Presented below is a set of independent situations. For each independent situation, indicate the journal entry to be made to record the transaction. Make sure that depreciation entries are made to update the book value of the machine prior to its disposal. (a) A fire completely destroys the machine on August 31, 2011. An insurance settlement of $630,000 was received for this casualty. Assume the settlement was received immediately. (b) On April 1, 2011, Chrysler sold the machine for $1,040,000 to Avanti Company. (c) On July 31, 2011, the company donated this machine to the Mountain King City Council. The fair value of the machine at the time of the donation was estimated to be $1,100,000.  Nordic Company, a merchandising company, prepares its master budget on a quarterly basis. The following data have been assembled to assist in preparation of the master budget for the second quarter. a. As of March 31 (the end of the prior quarter), the company’s balance sheet showed the following account balances: b. Actual sales for March and budgeted sales for April–July are as follows: March (actual) . . . . . . . $60,000 April . . . . . . . . . . . . . . . $70,000 May . . . . . . . . . . . . . . . $85,000 June . . . . . . . . . . . . . . . $90,000 July. . . . . . . . . . . . . . . . $50,000 c. Sales are 20% for cash and 80% on credit. All payments on credit sales are collected in the month following the sale. The accounts receivable at March 31 are a result of March credit sales. d. The company’s gross margin percentage is 40% of sales. (In other words, cost of goods sold is 60% of sales.) e. Monthly expenses are budgeted as follows: salaries and wages, $7,500 per month; shipping, 6% of sales; advertising, $6,000 per month; other expenses, 4% of sales. Depreciation, including depreciation on new assets acquired during the quarter, will be $6,000 for the quarter. f. Each month’s ending inventory should equal 30% of the following month’s cost of goods sold. g. Half of a month’s inventory purchases are paid for in the month of purchase and half in the following month. h. Equipment purchases during the quarter will be as follows: April, $11,500; and May, $3,000. i. Dividends totaling $3,500 will be declared and paid in June. j. Management wants to maintain a minimum cash balance of $8,000. The company has an agreement with a local bank that allows the company to borrow in increments of $1,000 at the beginning of each month, up to a total loan balance of $20,000. The interest rate on these loans is 1% per month, and for simplicity, we will assume that interest is not compounded. The company would, as far as it is able, repay the loan plus accumulated interest at the end of the quarter. Required: Using the data above, complete the following statements and schedules for the second quarter: 1. Schedule of expected cash collections: 2. a. Merchandise purchases budget: b. Schedule of expected cash disbursements for merchandise purchases: 3. Schedule of expected cash disbursements for selling and administrative expenses: 4. Cash budget: 5. Prepare an absorption costing income statement for the quarter ending June 30 as shown in Schedule 9 in the chapter. 6. Prepare a balance sheet as of June30.     |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

May 2021

Categories |

RSS Feed

RSS Feed